Auto suppliers are warning of slower order growth in the first half of 2026 as automakers adopt more cautious production strategies and adjust output to uneven consumer demand. The outlook reflects a broader normalization across the industry following years of volatility driven by supply disruptions and rapid recovery cycles.

Tier 1 and Tier 2 suppliers say order visibility has become less predictable. While automakers are maintaining production, they are placing shorter term orders and revising schedules more frequently. This has reduced the forward certainty suppliers rely on to plan capacity, staffing, and investment.

Executives point to demand uncertainty as a primary factor. Automakers are closely matching production to retail sales to avoid excess inventory, particularly in EV segments where adoption has slowed. That discipline is filtering through the supply chain, limiting volume growth even as overall production remains stable.

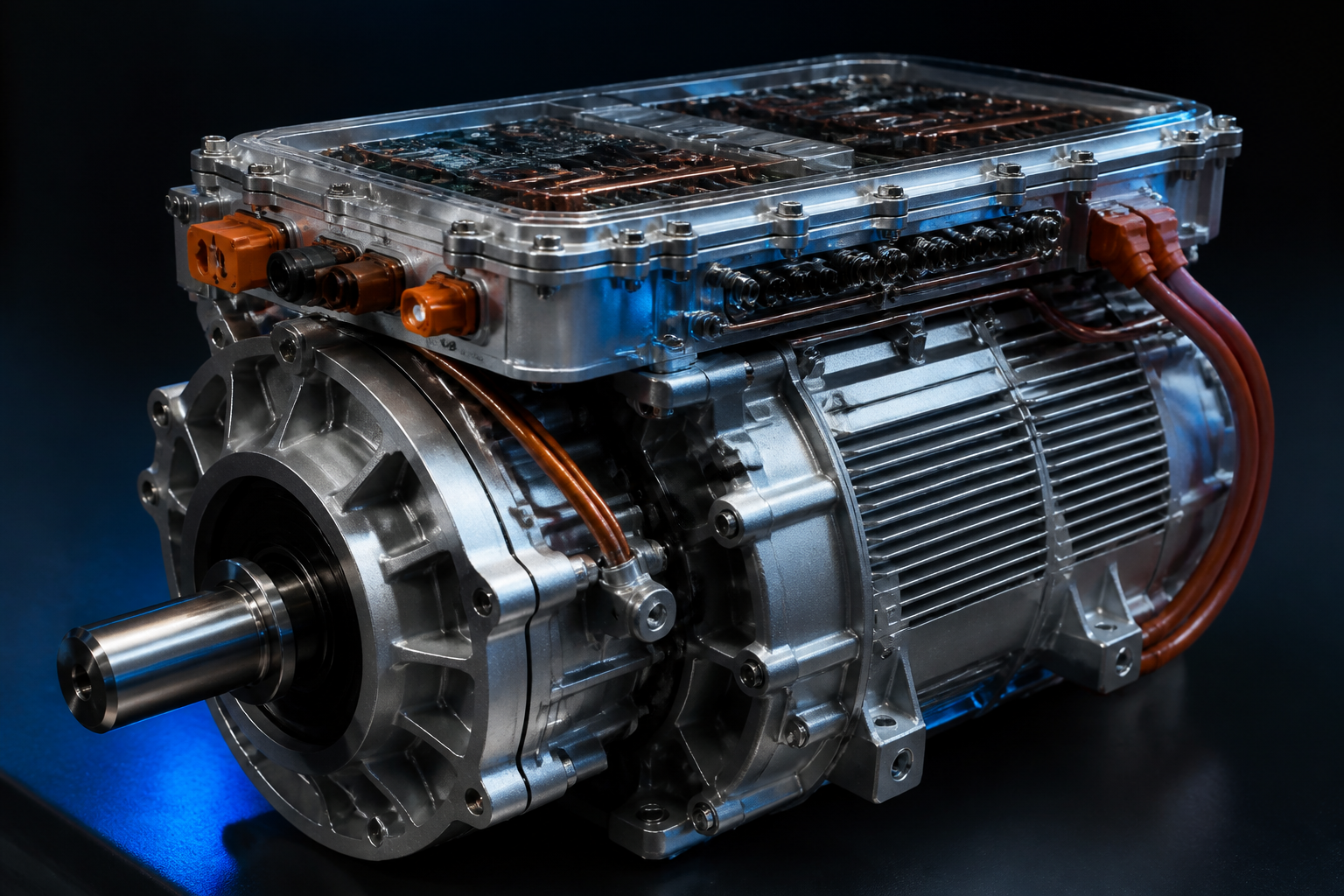

Electrification strategy shifts are also affecting suppliers. As automakers rebalance toward hybrids and extend the life of gas platforms, some suppliers are seeing delays in EV related programs while others experience steadier demand for conventional components. This uneven transition is creating winners and losers within the supplier base.

Pricing pressure remains a concern. Suppliers continue to face higher labor, energy, and material costs, but automakers are increasingly resistant to price increases. With margins already under strain, slower order growth reduces suppliers’ ability to offset fixed costs through volume.

Capital spending decisions are being reassessed. Several suppliers say they are delaying expansion projects, slowing hiring, and prioritizing efficiency improvements over growth investments. The focus is shifting from scaling up to protecting margins and cash flow.

Regional differences are also emerging. Suppliers tied closely to truck and hybrid programs report more stable demand, while those heavily exposed to certain EV platforms are seeing softer order patterns. This divergence is forcing suppliers to diversify customer and product portfolios where possible.

Despite the near term caution, suppliers stress that this is not a downturn scenario. Order levels remain healthy compared with pre pandemic norms, and long term demand drivers such as electrification, software integration, and advanced safety systems remain intact.

Industry analysts describe the first half of 2026 as a digestion period. After years of rapid change, the supply chain is adjusting to a market that rewards flexibility, cost discipline, and operational resilience rather than aggressive expansion.

For auto suppliers, the message is clear. Growth is slowing, but the industry is stabilizing. Those that adapt to lower visibility, tighter margins, and evolving product mix are likely to emerge stronger as demand patterns become clearer later in the year.